Weekly Thoughts by Mirabaud Securities - 3 May 2019

We were not used to it: The major US indices finished the week lower. Thanks to some profit taking but also to the Fed meeting. Despite his best efforts, Fed Chair Powell managed to spoil the party with his use of one of The Fed's favourite words - "transitory" - signalling that expectations for rate-cuts predicated on inflation staying low are perhaps not as set in stone as the market believes. The largest sectoral increases were due to real estate and financials. However, energy and communication services have lagged behind.

In Europe, it was the SMI that was the leader (thanks to the healthcare sector) and the FTSE 100 lagged behind (the rebound of the pound weighed heavily on the index). Finally, in Asia, we saw strong profit-taking in China over the week. In Japan, to mark the ascension of Japan’s new emperor, the government has declared an unprecedented 10-day holiday from late April to early May.

It’s quite unusual but over the week the Dollar was lower against 100% of G10 currency members. The British pound was the biggest gainer (in Dollar) ahead of the Norwegian Krona and the Euro. In emerging markets (still in dollars), the Argentine Peso grew by more than 3.5%, over Czech Krona and the Polish Zloty. The only significant decreases were the South-Coreen Won and the Indonesian Roupie.

Last year, oil prices rallied all the way up to a four year high before plunging more than $30. There were many factors at play during that volatile period, most notably the Iranian sanctions and the resultant promise by OPEC+ to boost production to avoid a supply shortage.

Since December 24th, WTI has gained more than 50% and we now think that over the medium term the best is behind us. Not only because of profit taking but also with uncertainty rife across a number of key areas in this year’s oil markets; demand, China’s economic health, global recession and financial turmoil, 2020 maritime regulations, trade war, production cuts, Iran waivers and of course the coming driving season putting pressure on the American president. As a reminder, Donald Trump is paying much closer attention to the harmful impact of higher oil and gasoline prices on consumers in swing states.

U.S. motorists consume almost 143 billion gallons of gasoline each year, according to the U.S. Energy Information Administration. Most is used by private motorists, though some is bought by businesses, governments, the postal service and the armed services.

Spain’s ruling socialists won the most votes but fell short of a majority in Sunday’s snap general election, a contest marked by the breakthrough of the far-right Vox party and a disastrous performance by the country’s traditional conservative party.

Pedro Sánchez’s Socialist Workers’ party (PSOE) won 123 seats, the conservative People’s party (PP) 66, the centre-right Citizens party 57, the anti-austerity Unidas Podemos and its allies 42, and Vox 24. Despite it being the country’s third general election in under four years, turnout was 75.8% – well up on the 66.5% two years ago. However, the PSOE will still need to seek the support of other parties to reach the 176 seats necessary to form a government in Spain’s 350-seat congress of deputies.

The upsides of the election are that Spain’s strong pro-European Union posture was not challenged, and that a stronger government under Mr. Sánchez should be able to tackle Spain’s neglected economic challenges. The election also demonstrated that extreme nationalism of the sort that has surfaced elsewhere in Europe is not yet a dominant force in Spain.

First, two quarters ago, Apple shocked investors when it said it would no longer disclose the number of iPhone it was selling - a clear signal that the selling was slowing dramatically. A few months later, on January 3 2019, Apple once again shocked the market when it slashed its revenue guidance by 8% for the first time ever. However, just like a quarter earlier, Apple's "shock" was quickly overcome, and the stock soared 46%.

This time there was no disaster, or even disappointment; in fact, the company reported Q2 numbers that beat across the board, while the company guided above the consensus range for Q3, and also announced a new $75 billion stock repurchase authorization. The company also announced that it is boosting its dividend to 77c/share from 73c/share. In short, ok numbers, but nothing breath taking, especially when one considers the company's guidance cut last quarter.

Several hot topics were discussed this 2 last weeks, including:

Oil in turbid water / Volatility at risk again / April Report Card / Fed meeting / Cyber attacks

Please feel free to ask for more information if interested.

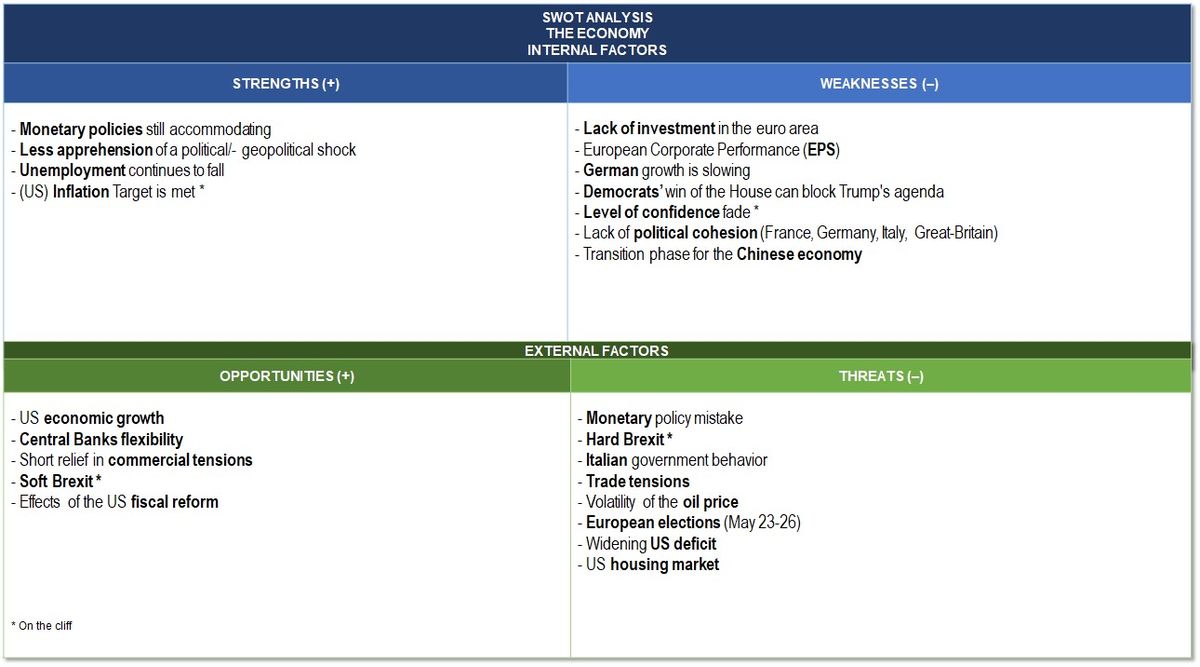

“(US) Level of confidence fade” (WEAKNESSES). Consumer confidence surged in February and rose for the first time in four months, a sign that Americans have regained optimism after the recovery in the U.S. stock market, the end of the government shutdown and diminished worries about recession.

“Hard and Soft Brexit” (Opportunities & Threats) is on the cliff this week after the Brexit was postponed to 31 October. There is still a risk, however, that the House of Commons will approve the withdrawal agreement before May 22nd.

SWOT stands for Strengths, Weaknesses, Opportunities and Threats, the French equivalent of FFOM analysis (Forces, Faiblesses, Opportunités et Menaces). While SWOT analysis can be used to develop a company's marketing strategy and evaluate the success of a project (by studying data sets such as company's strengths and weaknesses, but also competition or potential markets), I decided several years ago to adapt it as a way to analyse financial markets. SWOT analysis allows a general development of markets by crossing two types of data: internal and external. The internal information taken into account will be the strengths and weaknesses of the market. The external data will focus on threats and opportunities in the vicinity. Finally, and most interestingly, there is a table that will evolve according to current events, which will allow it to reflect the underlying trend in the financial markets on a weekly basis.

Please do not hesitate to reach out to your privileged contact person at Mirabaud or contact us here if this topic is of interest to you. Together with our dedicated specialists, we will be happy to evaluate your personal needs and discuss possible investment solutions tailored to your situation.

Author

Continue to